By Abdul Hamid bin Mar Iman1 and Mohammad Tahir Sabit bin Hj. Muhammad2

1 Univerisiti Malaysia Kelantan, Malaysia

2 International Islamic University Malaysia (IIUM), Malaysia

Cite as: Mar Iman, M. G. and Mohammed, M. O. (2020), "Animal Waqf as a Thrust of Social Entrepreneurship", International Journal of Management and Applied Research, Vol. 7, No. 4, pp. 411-431. https://doi.org/10.18646/2056.74.20-030 | Download PDF

Abstract

This paper is a foundation study on the concept of animal unit waqf (AUW). It is the first of its kind, based on local circumstances where there exists a need to encourage small farmers’ participation in animal husbandry in poverty-stricken and lack-of-employment states in Malaysia, through the concept of waqf. Understandably, poor members of the community who wish to raise animals as a source of living do not find an affordable means of beginning a herd. Livestock waqf could be offered as an approach to resolving this issue. Based on the concept of social entrepreneurship, this paper explores the mechanism of livestock waqf, in particular the bahīmatul an’ām, that could be introduced to the farming community in Malaysia.

1. Introduction

Agriculture is an economic backbone for many countries. It employs at least two billion people globally and directly supports the livelihood of 500 million smallholder farmers globally (World Bank, 2016). Currently, livestock is one of the fastest growing agricultural subsectors in developing countries making its share of agricultural GDP 33% (Thornton, 2010). The world now produces more than four times the quantity of meat as it did fifty years ago and 80 billion animals are slaughtered each year for meat (Ritchie and Roser, 2017). Out of these, the global cattle population is down from one billion in 2014 to 980 million head (Shahbandeh, 2020). This is about 0.71% of total livestock population.

Livestock farming in Malaysia is yet to progress to a higher level, especially utilizing idle land that can be converted to livestock farming. But, starting a livestock farm presents major obstacles for some of the younger generation because of financial limitations. Starting a livestock farm, in particular with cattle, is not within the reach of some poverty-stricken and unemployed members of the community in Malaysia. A couple of starter cattle can easily cost a farmer some RM 7-8K. The subsidy scheme called pawah system has now been limited to the rearing of small animals such as goat and sheep (Ismail., 1982; Ibhraim et al., 2016).

1.1. Rationale for animal waqf

Caring for animal welfare through waqf mechanism is generally an understood and accepted concept (Shaikh et al., 2017) and was practiced historically (Abdel Mohsin, 2019). However, making the animal itself as an object of waqf, i.e. donated as waqf, kept for breeding, and distributed to poor farmers or offered in the open market including as qurban, as well as being used for giving meat to the poor, has never existed anywhere in the world except for some rudimentary discussion in the classical books of fiqh. Our proposed model is different from the Global Wakaf model of Indonesia (Global Wakaf, 2016), which is restricted to waqf qurban or the supply of cattle for the purpose of qurban to Muslims by which the animal herd is sustained by replacement of old animals with young. While the Global Wakaf model manages the farm for the donors, our model looks at the reverse of this. The benefit of this model could be an addition to the model currently practiced by Global Wakaf. Indeed, it is time to consider this subject matter more seriously against historical practice and to compare contemporary practices more widely by focusing on the specific realization of waqf concepts to make it a potential strategy for strengthening socio-economic well-being.

The animal waqf system can help to improve the situation in the cattle industry in Malaysia which is troubled by being capital intensive, predominantly small-scale, and over reliant on imports of milk and meat. First, animal waqf strengthens and even improves the pawah system (a system with varied mechanisms whereby the government supplies live animals to farmers) in some aspects (see Ibhraim et al., 2016). Second, animal waqf encourages low-cost cattle farming where through animal waqf, qualified farmers receive live starter cattle for free which form the basis of a herd. Cattle-raising is the most under-developed industry in which Malaysia is facing the problems of milk and meat self-sufficiency. Third, the animal waqf system helps increase cattle populations in the long run through a greater participation of the community in cattle farming. Fourth, animal waqf system helps reduce dependence on imports of meat and milk. Fifth, it also helps lower retail price of the local meat. Sixth, animal waqf system can also help other members of the community with some form of food support via distribution of meat from the slaughtered animals. Last but not least, over a long period of time as the management capability progresses, the system can contribute to genetic preservation while supplying genetic resources to the livestock industry.

2. Social Entrepreneurship in Animal Farming

2.1. The concept of social entrepreneurship

By definition, entrepreneurship is the process of designing, launching, and managing business to encompass the capacity to identify business opportunity, acquire and deploy the necessary resources to develop and manage a venture with the associated risks (Johnson, 2020). It is basically a capitalist economic endeavor to enrich individuals who dare to take risks. But, in the last decade, attachment of social elements to entrepreneurship has become prominent to the extent that the concept of social entrepreneurship has received a lot of attention (Almarri and Meewella, 2015; Rostron, 2015; Mulyaningsih and Ramadani, 2017). Without going deeper into the debate on its very meaning, the philosophy of social entrepreneurship is associated with harnessing a range of socio-economic apparatus to capitalize social-oriented economic opportunities for sustainable living, which may be profit or non-profit based, and involved in commercializing services and products in order to sustain organizations (Rostron, 2015).

More than a mere socio-economic apparatus, waqf as a wealth distribution system for helping the poor and under-privileged has been enormously documented (Abdel Mohsin, 2019; Abdullah, 2019; Iman and Mohammad, 2014 and 2017). In this context, the contemporary waqf literature has promoted the theme of social entrepreneurship through a pool of articles on cash or non-cash waqf that has emerged over the past five years (Abdel Mohsin and Muneeza, 2019; Abdel Mohsin, 2019; Sherifah and Marhanum, 2020; Shulthoni et al., 2018; Iman and Mohammad, 2014). From these works, the obvious similarities between social entrepreneurship and waqf lie in their focus on enterprise, social development, social well-being and prosperity. Contrary to general misconceptions, waqf is not only a charity but is an enterprise. Waqf shares its objectives with social enterprise in addressing social, economic, and environmental problems that constantly need innovative methods of income generation. In this context, waqf prioritizes its total net income and proceeds derived from its products and services, to be given to society. In the process, financial sustainability forms the core of waqf, particularly in the Hanafi School. The waqf system endeavors the growth of funds, widening entrepreneurship activities, earning profits, while sustaining an inflow of new donations.

With recent studies suggesting the utilization of non-land resources for creation of new awqaf in Muslim communities, animal farming as a form of social entrepreneurship is yet to receive any serious attention. As a type of chattel, animals raised on farm are capable of yielding various forms of benefit to society. Its charity causes can be promoted among the general public with the opportunity to reap handsome rewards for the Hereafter – a very vital aspect of practicing tawhīd and ‘ubudiyyah towards God Almighty, and making the waqf institution contribute to the five objectives of shariah as well benefitting humanity in general based on the higher objectives of the religion of Islam, particularly socio-economic equality and justice (Iman and Mohammad 2017). This philosophy of waqf makes it clear that the relationship with God Almighty and relationships with people are equally emphasized as an act of piety. And this is a silent philosophy of social entrepreneurship which is in line with Shariah law.

2.2. Fiqhi foundation of social entrepreneurship

As understood from the above discussion, Islamic social entrepreneurship through waqf would mean the establishment of a new and innovative charitable organization financed by faith-based donations, dedicated to income-generating processes, wholly and in perpetuity to sustain itself financially and to address social, economic and environmental needs of society.

The source of capital of an Islamic social entrepreneurship (ISE) is charitable funds. Though it is voluntary, the driver of donation is faith based, as it is indirectly implied in the broad concept of charitable deeds found in the Glorious Qur’an and the Sunnah of Prophet PBUH. These are such as goodly loan (Al-Baqarah: 245), sadaqah (Al-Baqarah: 177, 215, 245, 254, 261; Āli ‘Imran: 92, 133; Al-Anfāl: 3, 60; Al-Ahzāb, 35: al-Munafiqūn, 8-9; Al-Tawbah; 60, 99, 103), al-birr (Al-Nisā’: 92; Āli ‘Imran: 92), generosity (Al-Taghābun: 17, Al-Isrā’: 28), and wealth re-distribution (Al-Baqarah: 215, 264, 270, 280). The Sunnah of the Prophet PBUH also asserts the same concepts. Abu Hurairah r.a. reports that the Prophet PBUH says: “When a man dies, all his acts come to an end, but three: recurring charity, or knowledge (by which people benefit), or a pious offspring, who prays for him” (Sunan an-Nasa'i 3651, Book 30, Hadith 41). In another hadith, Abu Hurairah r.a. also said that the Prophet PBUH says: “If someone gives charity with a fair date from a good earning - and God accepts nothing but the good - verily God accepts it with His right hand and then raises it to its owner as one who raises it so that it is like a mountain” (Al-Bukhāry, Kitab al-Zakāt, Hadith No. 1410).

Although the terms social entrepreneurship, in the sense of focus on socioeconomic and environmental problems, were only coined up in the last ten years or so, dedication of the capital and net income of a business to the socioeconomic problems of society was already embedded in the concept of waqf since the time of Prophet PBUH (Al-Khassaf, d. 261 H). Now, the term Islamic social entrepreneurship (ISE) enters the body of knowledge on waqf. By definition, Islamic social entrepreneurship (ISE) is a welfare system for capitalizing social-oriented economic opportunities through entrepreneurial activities that are guided by the Islamic principles. Within its definition, ISE has spiritual, socio-economic, and entrepreneurial dimensions (Almarri and Meewella, 2015; Mulyaningsih and Ramadani, 2017). The spiritual dimension is built upon the Muslim philosophical concept of linking material issues with spiritual convictions (tawhid), provided under religious laws (fiqh of ibādah), and Islamic objectives (maqāsid al-shariah), and perpetual charity (sadaqah jāriah); the social dimension is designed on the concepts of Islamic solidarity (ta’awun) and equity (al-‘adl) similar to Ibn Khaldun’s economic concept discussed under theory of belongingness (‘asābiyyah). While the entrepreneurship dimension is built upon the Islamic law of gifts (fiqh of muāmalah) the notion of wealth and the structure of market is derived from the practices established during the time of Prophet Muhammad PBUH, as can be seen from the waqf market activities in different countries, revived, innovated, and practiced within the last four decades.

The creation of animal waqf as a thrust of social entrepreneurship does not contravene the Shariah law as long as it fulfils the fiqhi principles of waqf in raising capital for the enterprise while being shariah-compliant in its market activities. Animal waqf as it is seen here widens the scope of business activities of waqf, and adheres to the governing rules of shariah on raising waqf capital, its preservation, and maximization of income to be spent on management expenses of the waqf and distributed to the beneficiaries of the waqf.

The origin or capital of waqf has its firm footing in Islamic law based on the social goals of Islam, i.e. surrendering one’s coveted possession in the path of Allah for improving society’s well-being (see Iman and Mohammad, 2014). For example, waqf is used as a social tool that not only finances business enterprises for the needy but also employs poor and underprivileged groups through its accumulated capital (Abdel Mohsin, 2019; Iman and Mohammad, 2017), income and preferably businesses operations.

The explanation of al Khassaf, (d. 261 H., p. 29), and Ibn Al-Fara, (4: 511) takes the concept of waqf further to be included in the normal market activities as they allowed waqf of the non-Muslim and waqf on the rich and non-Muslim, provided it is for lawful social objectives (Al-Khatib and Al-Bujairimi, pp. 242-249; Al-Mawardi, p. 118). Muslim jurists insist on self-sustainability of waqf institutions by requiring perpetuity of the capital and/or its object (cause) as well as by perpetualisation through maximization of income and aversion to risky market activities. The latter is inferred from their view on enforcement of business agreements and dealings of the trustees of waqf, whenever such clashed with the perpetuity of the subject or object of waqf, and prioritization of the subject over its object in cases where the income of the business (agricultural, real estate, and cash economy) was affected by poor management, and market trends.

2.3. Fiqhi foundation on animal waqf

The many types of benefit of animals are mentioned a number of times in the al-Quran. Two of these are revealed in surah al-Mu’minoon, verse 21: “And for you in the livestock is some lesson – we give you drink from what is in their bellies and you have many benefits in them and from them you eat. And on them and on the ships you are transported” and in surah al-Nahl, verse 66: “And for you in the livestock is some lesson – we give you drink with what is in the belly of each of them (while) between the dirt and the blood is pure milk that is clean for the drinker.”

Two key constructs immediately strike one from these Quranic verses, namely the benefit of something and the perpetual flow of the benefit. Hidden in the meaning of these verses is that the benefit of the animals can flow perpetually if they are raised under sustainably. Indeed, the perpetual flow of benefit is an important principle and a condition of waqf. For example, a piece of land or a situs location can be given away permanently to produce sources of physical materials for the community such as water, fruits, grains, and animals.

A question is now asked: can livestock, in particular bahīmatul an’ām, be made an object of waqf? [Bahīmatul an’ām is common four-leg livestock animals in the category of ruminant such as camel, buffalo, cow, sheep, and goat.] Any decision on permissibility must be based on clear fiqhi rulings, particularly how it satisfies the conditions of a waqf. Unfortunately, the issue of livestock waqf is less definitive among the four schools of law; its contentiousness and the lack of literature debate makes the concept rather fragile at least for now.

An animal without an identified owner is not allowed as waqf while that with a clear ownership raises some controversy among the classical jurists about its permissibility. The disagreement among the classical scholars is cited in detail in Ibrahim (2007). Al-Daarimi did not allow it while al-Dubliy did allow it (Al-Nawawiy, d. 272 H, p. 382). Al-Tabari allowed livestock waqf while Quzwaini himself was slanted towards its non-permissibility (Al-Quzwaini, d. 623 H, p. 256). Al-Bujairmi (d. 1221 H, p. 619) was considered by some people as not allowing waqf of bahīmatul an’ām while perceived to be silent on it by some others. Ibn Hajar was against animal waqf (Al-Syarwāni and Al-‘Ibādi, n.d., pp. 243-244). Some scholars ruled that animals used for transportation or riding can be made waqf (Al-Juwaini, d. 478 H, p. 148). Further, almost all rulings did not specify the detailed fiqhi principles for or against the waqf of bahīmatul an’ām. Therefore, we suggest that the controversy over waqf of bahīmatul an’ām be viewed from the perspective of Imam Al-Shafi’e in his treaty on waqf or sadaqat muharramat and those who follow him strictly to the letter.

The leading Shafi’e scholars agree on the permissibility of waqf of movable property. Imam Al- Shafi’e differed from Imam Muhammad in his debates with him, on the waqf of slave men based on the short life of humans or being lost (Al-Shafi’e), therefore rejecting the concept of perpetuity (ta’bid) of waqf property maintained on by Imam Muhammad. Imam Al-Shafi’e, clearly did not intend the waqf property to be perpetual or landed as was the opinion of Imam Muhammad from the Hanafi school of law. Imam Al-Shafi’e and Imam Abu Yusuf agreed on the waqf of moveable properties based on the Sunnah of the Prophet PBUH.

The view of Imam Shafi’e is clear: anything that can be identified and be observed by witnesses, such as camels, cows, and sheep can be donated as waqf. Therefore, the waqf of animals (mashiyah) is valid. Al Shafi’e expressly rejected the view of Imam Muhammad and other Hanafi Imams on permission of animals if they form part of agricultural land or buildings, for being not perpetual. Imam Shafie does not see perpetuity of the subject matter of waqf for he does not see perpetuity in land and buildings too. Like slaves, animals and land can also be subject to an Act of Allah that could make the land unusable, Imam Shafie wrote.

Nevertheless, Imam Shafie did not allow revocation of waqf. This is to say once the object is donated, the declaration is binding automatically, and the waqif has no power to deal with it anymore. This includes the power to revoke the declaration. Waqf then become perpetual. Similarly, Imam Shafie permitted waqf to be on such an object and purpose that can exist perpetually. Therefore, any waqf on specific persons must be followed by those that can be specified by a class of them that can exist perpetually. If the donation is declared in such way that indicates that the beneficiary of the waqf may not exist for long time, Imam Shafie considered such declaration revocable. Thus, the followers of the Imam have taken irrevocability and perpetuity of the object fundamental elements for the validity of the waqf. This makes the waqf of Shafie different from that of Imam Muhammad. The latter believed in the perpetuity of the property and declaration while the former believed in the perpetuity of the object i.e. the beneficiary, and irrevocability of the declaration. What they disagreed upon was the perpetuity of the property. Hence the waqf of animal as an original waqf is valid according to Imam Shafie and according to Muhammad and other Hanafi scholars, waqf of animal can be valid if they are part of the farmland.

The most important principle of waqf is to keep the corpus intact and to give its produce as sadaqah (Abdullah, 2019; Iman and Mohammad, 2014). This principle is rooted in the Hadith of Prophet PBUH (al-Nasāi’, d. 303 H; al-Baihaqī, d. 457 H). The corpus is the object (e.g. land and chattels) while the produce is the benefit of a waqf. In this context, Imam al-Shafi’e has pointed out that ”…the object or the cause of waqf owns its ‘fruits’ not what is freed...” (Al-‘Imrāni, d. 558 H, p. 75). In the case of Khaybar land belonged to ‘Umar al-Khattab r.a., what was freed of his personal possession (the land) resulted in ‘fruits’ obtained therefrom, which were the agricultural proceeds that were released to be distributed to the society. Abu Hurairah r.a. also reported that ‘Umar al-Khattab gave away armour and gears – as movable assets – in waqf after receiving an advice from the Prophet PBUH about giving sadaqah (Sahih al-Bukhari, Hadith no. 1468; Sahih Muslim, Hadith no. 983). Al-Syatri (2008) commented that this hadith is a proof that waqf of a movable asset is allowed in Islam as long as its benefit is given away to flow in His path. Imam al-Shafi’e, in particular, allowed immovable as well as movable assets such as house, land, clothing, furniture, warfare tools, and animal as waqf (Al-‘Imrāni, d. 558 H.).

Like any other animals, cattle can multiply by maintaining or improving its progeny lines. In the case of animal waqf, the object of waqf (cattle) owns the continuous flow of off-spring which are produced from a specified minimum size of AUE of known breeds and gene (nasl) of cattle. Scientific evidence has it that animal’s progeny can be maintained for an indefinite time period with possible transmission of attributes based on the type of breed. Such attributes are inherently maintained in the gene. Genes, progeny lines, and the associated traits in an animal are inheritable and, thus, are long-lived. By implication, tafriqat al-nasl comprises two closely related breeding elements, namely breeding path and herd expansion (see Section 4.2.2). These require professional animal farm management, including the scientific application of breeding programs.

3. Animal Unit Waqf

This section is important because it provides a basic explanation of the technicalities of an animal unit waqf, the shariah compliance of its framework, and the managerial functions of the team working for the growth, maintenance, and sustainability of the animal waqf farm in an integrated manner.

Animal unit waqf (AUW) is a dedicated unit of what is termed as animal-unit-equivalents (AUE) entity of stipulated type, conditions, and of shariah-sanctioned livestock animals (halal and mal mamlukah) called bahīmatul an’ām, for their natural life time and replaceable by other similar animals, be they from the offspring of the original animal or otherwise, to which the public are invited to donate for an unceasing or perpetual specified cause and object, as an act of piety to the God Almighty. AUE waqf unit is basically a quantity-and-quality based physical stock of animals raised on a farm over a particular time period, usually annually, but which is monitored as value-based entity to which it dynamically suits its physical-value relationship according to market changes. Configured in this way, AUW can be designed to conform to the pillars of waqf. The concept of AUW is illustrated in Figure 1.

In figure 1, the AUE waqf unit is derived from a cattle population to which the public donate live cattle. The management team of AUW will invite public on ad hoc manner, or systematically, from time to time, to increase the pool of livestock dedicated as waqf. Once the donation is collected donors will have no control over its management, or its income, or could benefit specifically there from. For a good management purpose, though, donors could receive the annual report of the activities, financial management etc. of the farm.

This AUE waqf unit has to be managed and maintained by the AUW management team as an infinitely long-term “pool” of animal stock including the donated ones and their produce. Two-level farm management would be carried out to raise the animal; the first level is on the waqf farm while the second-level is on individual locations to whom the produce of the donated animals will be given in stages. Apart from being distributed to poor farmers, some will be sold live slaughtered, etc. the surplus product or proceeds of which are channeled to poor and needy beneficiaries. Meanwhile, animals distributed to individual farmers will be individually managed further, multiplied, and finally harvested for income by the farmers themselves.

AUE waqf unit is a new concept and, because of this, contention and controversy against its concept and implementation are expected to surface for time to come. However, further studies that can shed more light on its concept and practice will be able to strengthen its concept before it is accepted to become a new innovative waqf system. Nevertheless, we are of the opinion that this is in line with what was proposed by Al-Juwaini (d. 478 H, p. 148) that for animals raised for production, their permissibility as an object of waqf must be investigated in detail.

We argue that, to comply with shariah principles of waqf capital, the AUE estimate for each donated animal can be conveniently determined based on two main criteria, namely animal age and its position in a cow’s breeding cycle. This is illustrated in Figure 2. A normal cow passes a period of 30 months from first being a ready-to-mate cow till heifer-born weaned calf. Since the physiological and health conditions of an animal may change during this period, the AUE concept is used to assess each animal donated to the waqf farm.

Animal unit is a standard measurement of a 1,000-kg mature bull (1.5-2.0 years old) grazing on paddock that consumes a certain amount of grass. From this, we derive what is called animal unit equivalent (AUE) to comply with shariah principles. Table 1 gives a general guide on assessing animal unit. In the figure, all categories of animal make up AUE = 4.27 on the basis of Table 1. The actual AUE that can be obtained on a AWF will depend on public donation of live animals. The appropriate desired AUE on the farm will need to be determined by the management team and this will become its strategic target in a particular year. The market value of each of the animals will also need to be estimated at the current market price.

| Animal class | AUE |

|---|---|

| Bull, mature | 1.35 |

| Cow, 1000 lbs., with calf | 1.00 |

| Cow, 1000 lbs., dry | 0.92 |

| Cow, 2 years old | 0.80 |

| Cow, 1 year old | 0.60 |

| Sheep, mature 0.20 | |

| Sheep, bighorn, mature | 0.20 |

| Lamb, 1 year old | 0.15 |

| Goat, mature | 0.15 |

| Kid, 1 year old | 0.10 |

3.1. The working model

The concept of AUW shown in Figure 1 is further illustrated in Figure 2. The grey-shaded items with the solid arrows in Figure 2 represent the core components of animal waqf model while the dotted lines represent the auxiliary relationship between AUW mechanism and external factors such as the waqf unit’s management, market or industry, and other stakeholders. The nucleus of AUW consists of a perpetually maintained animal unit (MAU) based on maintained animal unit equivalents (AUE), grazing land, infrastructure, buildings, and facilities, which together form an animal waqf farm (AWF). The AWF would initially be financed with two main sources of dedication, namely the general public’s donation of feeder cattle and/or AWF-dedicated cash donation to be used for purchase of new breeders or feeders, land, and equipment and management operations.

The management would have the power to maintain the AWF, reserve produce and cash, trade in the produce of the farm, and distribute specific produce to the poor and needy. The donated animals or purchased by cash waqf later need to be replaced from its produce or purchased with income. Live-animal replacement would be regularly carried out via a specific breeding program on the farm. The distribution of the produce can be made to the poor either by giving live animals or meat. Farmers would receive a pair of male-female starter breeders free of charge but would undertake to return them or their progeny to the AWF, according to the stipulated terms and conditions.

To ensure the perpetuity of the AWU as well as AWF and to counter foreseeable as well as unexpected risks to the farm (e.g. death, sickness, loss of animals due to theft or other events), the manager has to devise a good farm management plan for the replacement of original animals. In other words, live animals and cash have to be reserved for this purpose. Apart from the farm’s deferred operating profit, among the strategies to ensure a successful replacement program is to encourage the public to give live animals or AWF-dedicated cash donations through constant marketing campaigns and incentives. From time to time, market monitoring is required to ensure value-based control of the MAU. In general, value-based monitoring is carried out to ensure that the value of per unit MAU is not fluctuating too much over time (see Section 3.3. value-based waqf).

3.2. Components of AUW

Can animals be an object of waqf while the land is not? With regards to cattle as an object of waqf, a Hanafi scholar al-Khassaf (d. 261) based on the opinion of Imam Muhammad made a ruling that: “...it is not allowed to make waqf of a slave without the land, but if he makes waqf of the land forever for the sake of Allah... and the slave is working on it, it is permissible ... If there are also cattle on it where he specify their number he has to stipulate in his charity that the expenses of the slave and the cattle be taken from the proceeds of the land ...” (p. 152). According to him, making waqf out of cattle should be done together with the land on which the animal grazes. However, Imam Shafi’e specifically rejected this rule and allowed the waqf of live animal without attaching the condition mentioned by al-Khassaf.

Imam Shafi’e and Imam Abu Yusuf agreed on waqf of moveable properties based on the Sunnah of the Prophet (PBUH). Anything that can be identified and be observed by witnesses, such as camels, cows, and sheep can be donated as waqf. Therefore, the waqf of animals (mashiyah) is valid (al-Shafi’e, d. 204, 5: 120). Therefore, declaring the land on which the animals are raised as waqf is preferable, but it should not be made mandatory. This is because, if the land ceases to be waqf, the whole farm operation has to be closed down whereas the animals and the equipment can be moved from one place to another. For this reason, the permissibility of establishing a farm on leased land can still be a choice, especially where finding waqf land is difficult.

By taking the positive side of the above argument, we are of the opinion that animal waqf be allowed conditional upon the following requirements:

- the herd is maintained on the basis of the stipulated AUE which is reasonable on the basis of management capacity.

- the actual composition of animals on the basis of AUE should be adjusted, from time to time, based on the concept of value-based waqf.

- the mutawalli has the intention, undertakes, and provides proofs of the necessary efforts for long-term farming; and

- the management can ensure the flow of tangible benefits from raising the animals based on its farm management plan.

The details of the value based waqf are discussed below.

3.3. Value-based waqf

Iman and Mohammad (2014) proposed the concept of value-based trust. This concept in simple words argued for declaration of the value of a waqf asset. Real estate or any accepted movable property should be valued at the time of the declaration and through good management the ascertained market value has to be maintained in perpetuity. This concept is prerequisite for ascertainment or determination of animal unit equivalent and its maintenance through proposals discussed in section 4.

Value-based waqf was proposed to develop flexibility of waqf and to mitigate the hardship caused by the concept of perpetuity of the subject matter of waqf (mawquf) in the Hanafi School of law. For the followers of Shafi’e school, perpetuity of the purpose of waqf (mawquf ‘alaihi is not the condition, and therefore, value based waqf should not be an issue. The proposed concept merely provides an alternative where one is concerned with price stability of the waqf asset in the market and to measure the growth of waqf assets. However, value-based waqf has not been widely discussed.

The main argument for value-based waqf is that if any chattels can ensure a perpetual flow of benefits in terms of value then they can become an object of waqf. For that matter, if a particular type of bahīmatul an’ām can be managed as an enterprise in such a way so as to yield a continuous flow of benefits while at the same time preserving certain level of maintainable value then they can become an object of waqf. By this principle, it is permissible to reap benefits from the livestock in whatever forms that is consistent with the shariah.

To limit our topic in this paper, we just focus on cattle as an example, though the concept can be used for other types of livestock farm. By breeding cattle on a farm, the animal will multiply, the herd size will grow, and, over time, there will be age and sex composition of animals – bull, heifer, stock, calf, etc. Some of them are to be kept as stock, replaced from time to time from offspring and kept for their produce, while the replaced animals and others can be harvested for meat, milk and other uses. Under good sustainable farm management, the herd can last for an infinite period or at least over a long period of time.

Under the concept of value-based waqf, AUE growth (AUEG), usually per period, is vitally important. It is a figure that quantifies how much the original EAUE has increased to the next-level on the basis of herd size over a given period of time. For example, from the original EAUE of 4.03, the herd grew to a size of 13 head of cattle in five years. The AUEG was therefore equal to (13/4.03)/5 = 0.625 per annum. Such a figure has an important role especially indirectly measuring animal, herd, and management performance.

Let say, during the five-year period, due to market dynamics, animal-unit value was fluctuating (in our case, between RM 14,000 and RM 56,000 with AUE standing between 3-5). This means, per animal-unit value could have been fluctuating between RM 4,666.67 and RM 11,200 over the period. Such a fluctuating situation cannot become a good basis for waqf because an object of waqf ought to be not volatile. Rather, a stable value based AWU should be envisaged. This is done by stipulating a minimum MAU. In Figure 3, this is indicated by the horizontal broken line set, say, at a level of 5.0 for the next five years.

In order to catch up with the fluctuating AU value curve, improvement in animal units can be made by one of two approaches. First, increasing the slope of AUE curve (steeper AUE curve1) resulting in a higher rate of AUE growth. This is done by improving farm management such as grass quality, concentrate quality, increased mating frequency, etc. Second, shifting the AUE upwards (from AUE curve0 to AUE curve2) by harnessing factors such as better production technology, superior breeds, improving herd composition and size, and structural market adjustment.

From para 4.1 and 4.2 it is obvious that a 4.03 AWU is capable of producing about 28 young animals over a five-year period. This is considered a small size of herd and may not be able to serve to the community satisfactorily. To allow for a bigger size of animal herd say, 100 head of animals, the AWU should be expanded to 4.03/28 x 100 ≈ 14. However, such a size of animal herd should be carefully assessed by the management team. If this is within the capacity of the AWF’s management team, in terms of available resources then this should be declared as the targeted MAU. Then, it should be declared to the public for the purpose of initiating waqf and inviting participation of animal donors. This shall continue to grow until a time when the need of society is satisfied, not only in term of supply farm products but also bringing fair farming in the country for the employees and clients of the farm.

4. The Case Study

4.1. Mock AUW

The case study has a vital managerial value as it illustrates the role of breeding science in animal waqf management. It illustrates how the management can establish, grow, and maintain financial sustainability through reserves, distribution of the produce, and income from the waqf. It involved ‘mock waqf’ animals obtained from five local individual donors in 2015. They comprised one 1.5 year old Hereford starter bull (S) and five 1.31-average year old Hereford heifers (H1, H2, H3, H4, and H5) with an estimated AUE (EAUE) of 4.03 (Table 2).

| Breeder | Donor’s locality | Delivery live weight (kg) | Age at delivery (year) | Breeding stage | EAUE* |

|---|---|---|---|---|---|

| Bull (S) | Tanah Merah | 248 | 1.50 | Starter | 0.83 |

| Heifer (H1) | Tanah Merah | 210 | 1.29 | Dry, parity 0 | 0.70 |

| Heifer (H2) | Tanah Merah | 185 | 1.35 | Dry, parity 0 | 0.62 |

| Heifer (H3) | Tanah Merah | 187 | 1.33 | Dry, parity 0 | 0.62 |

| Heifer (H4) | Jeli | 190 | 1.26 | Dry, parity 0 | 0.63 |

| Heifer (H5) | Jeli | 188 | 1.31 | Dry, parity 0 | 0.63 |

| Total = | 4.03 |

EAUE = (1.43/WAUE) x WA x FA

Where EAUE = estimated animal unit equivalents; WAUE = stipulated weight that equates to 1.0 animal unit equivalent; WA = actual weight of a given animal; FA = adjustment factor for age, A (x 1.0 if A = 15% x 1.5-2.0 years old). [Adjustment for A was rather judgmental but it can be further analyzed based on a scientific study.]

The natural breeding process took place on a piece of land near Universiti Malaysia Kelantan campus at Jeli. Animals were raised semi-intensively with irregular cut-and-carry system. Animals were largely grass-fed with minimal supervision. This kind of management regime was purposely chosen in this study to simulate productivity r under a ‘passive’ management regime – a predominant scenario among small, part-time cattle farmers in Malaysia.

4.2. Breeding simulation

Underlining the sustainability of animal waqf is the tafriqat al-nasl itself that configures the success of any breeding program. However, a detailed discussion on breeding is beyond the scope of this paper. By principle, tafriqat al-nasl is necessarily preceded by the determination of breeding path and the strategy for herd expansion. Both then determine animal unit multiplier. Breeding simulation of the pioneer group was carried out to determine the possible outcome of AUW based on the performance of the basic breeding factors. An actual experimental study over a certain period of time is required to obtain the actual field results of these factors. In this study, only two-cycle breeding period (5 years) was used for the simulation (see Figure 4).

4.2.1. Breeding path

Besides a sufficient number of steers, a farm needs to have more number of heifers since the productivity of the herd depends largely on the number of heifers available for mating. From each breeding cycle, 50: 50 chances of getting male-female off-spring was expected. Further breeding activities should be well managed to yield further generations of cattle.

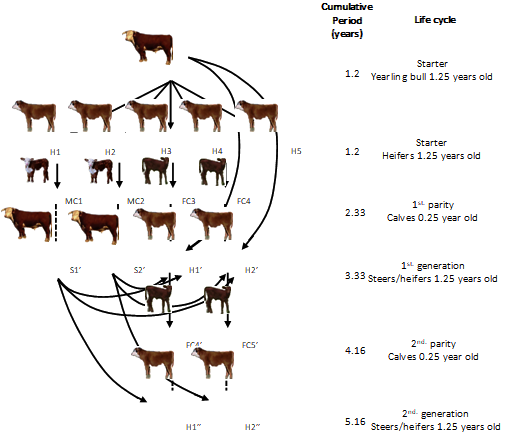

Figure 3 shows the breeding path of a Hereford yearling bull (S) and five Hereford heifers (H1-H5) that have just reached puberty. It shows two-generation breeding cycles of cattle with the original EAUE of 4.03. The S x (H1-H5) mating was conducted over a 1.5-month bull-run period. Under a constant supervision, S x (H1-H5) mating was carried out in turn at each heifer’s earliest heat signs (US Food and Drug Administration, 2019). The heifers gave birth 280-285 days from their first conception.

The first-round natural mating was 80% successful with one heifer failing to conceive. Four calves (MC1 and MC2 males and FC3 and FC4 females) were born. In the second stage, the original yearling bull (S) was mated with now-heifer FC3 and FC4, i.e. H1’ and H2’. As a “training”, now-steer MC1 and MC2, i.e. S1’ and S2’ were mated with the second-generation heifers (H1” and H2”). This process continued until the original bull (S) was old enough for culling. In Figure 3, the “old” bull was culled at the age of about 5 years old. Normally, such an animal would be slaughtered and meat distributed to the local poor and needy. Some of the young but less productive or not-for-breeding animals (e.g. steers and heifers) can also be culled while the productive ones sold as feeder or breeder cattle. Some of the selected steers are kept as bulls for further breeding.

By the principle laid out in the Shafi’e madzhab, S, H1, H2, H3, H4, and H5 should be maintained as the original waqf but since they will cease to exist after some time, they must be replaced by new individuals. The rate of replacement depends on many factors such as the number of donated breeders to farmers, traded live animals, culling, death, unproductive individuals, etc. Therefore, apart from continuous donation from the public and female-calf return from the participating farmers, professional animal management is necessary to ensure that animal breeding is performed in the best manner to ensure the sustainable number of animals to maintain the minimum AWU. Besides, from Figure 2, the Waqf Unit will use some of the financial proceeds to purchase new breeders to add to the existing stock.

4.2.2. Herd expansion

Figure 4 illustrates the various possible ways of breeding path that can be chosen by farmers. It depends on which animals and breed lines are being mated. Table 3 and 4 illustrate the simulation outcomes of mating options as illustrated in Figure 3.

| Animal | Pioneer breeders’ age (years) at early period of | Number of animals | Revenue at culling age (5 years) | ||||

|---|---|---|---|---|---|---|---|

| First mating | 1st. generation calves | 1st. generation steer/heifer | 2nd. generation calves | 2nd. generation steer/heifer | |||

| S | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 7,500.00 |

| H1 | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 8,000.00 |

| H2 | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 8,000.00 |

| H3 | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 8,000.00 |

| H4 | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 8,000.00 |

| H5 | 1.25 | 2.33 | 3.27 | 4.04 | 5.29 | 1 | 8,000.00 |

| S1 | 1.25 | 2.02 | 3.27 | 1 | - | ||

| S2 | 1.25 | 2.02 | 3.27 | 1 | - | ||

| H1 | 1.25 | 2.02 | 3.27 | 1 | - | ||

| H2 | 1.25 | 2.02 | 3.27 | 1 | - | ||

| H1 | 1.25 | 1 | - | ||||

| H2 | 1.25 | 1 | - | ||||

| S x with | S1’ x with | S2’ x with | |||||||||||||

| Year | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 |

| Age | 1.25 | 2.06 | 3.06 | 4.06 | 5.31 | 1.25 | 2.25 | 3.25 | 4.25 | 5.25 | 1.25 | 2.25 | 3.25 | 4.25 | 5.25 |

| H1 | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | - | - | - | 1st. m | ✓ | - | - | - |

| H2 | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | - | - | - | 1st. m | ✓ | - | - | - |

| H3 | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | - | - | - | 1st. m | ✓ | - | - | - |

| H4 | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | - | - | - | 1st. m | ✓ | - | - | - |

| H5 | 1st. m | x | ✓ | ✓ | Cull | 1st. m | ✓ | - | - | - | 1st. m | ✓ | - | - | - |

| H1’ | 1st. m | ✓ | Cull | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | ✓ | ✓ | Cull | ||

| H2’ | 1st. m | ✓ | Cull | 1st. m | ✓ | ✓ | ✓ | Cull | 1st. m | ✓ | ✓ | ✓ | Cull | ||

| H1’’ | - | - | - | - | - | 1st. m | ✓ | Cull | 1st. m | ✓ | Cull | ||||

| H2’’ | - | - | - | - | - | 1st. m | ✓ | Cull | 1st. m | ✓ | Cull | ||||

| Total calves | 4 | 5 | 7 | 7 | 2 | 4 | 7 | 2 | 4 | ||||||

| Cumulative* | 4 | 9 | 16 | 29 | 7 | 9 | 11 | 27 | 7 | 9 | 11 | 27 | |||

Note:

Assuming 80% calving through S x (H1, H2, H3, H4, H5) in the first year.

*The number of calves reflects a maximum of 80% breeding success.

Each mating pair results in one calf born. ✓ indicate the live calf.

The breeding matrix shows the potential generation of calves using three alternative steers, namely the parent stock, S, and the second-generation steers – either S1’ or S2’. The farmer decides to dispose of the steers when they reach the age of about 5 years old for a number of reasons. First, he does not want to wait for too long to harvest an ‘old’ animal; 5 years is considered to be long enough. Second, to avoid cost overrun due to maintaining an older herd. Third, declining productivity and meat quality. Fourth, lack of demand for older animals.

With any choice of the three steers, the farmer chooses to mate all-generation heifers with the aim of getting the most productive outcomes. Tables 3 and 4 show that about 27-29 young animals can be bred in five years.

4.3. Distribution of benefits

As illustrated in Figure 2, there are a number of benefits that can be generated from the animal waqf scheme which can be channeled to society. Table 5 shows the main management decisions on the waqf benefits once the cycles of breeding are completed. In this study, only ‘cull and meat distribution’ was simulated with the first six pioneer cattle (S, H1, H2, H3, H4, and H5. With the estimated average meat output of 815.10 kg from the slaughtered animals and 2-kg of meat distribution per family, at least as many as 410 needy families can be helped with food support program.

| Decision | Animal ID | Quantity | Estimated output (kg) | Estimated no. of beneficiary (Local poor families) |

|---|---|---|---|---|

| Cull and meat distributiona | S, H1-H5 | 6 | 815.10 | 410 |

| Live animal distribution b | - | - | - | - |

| Semen distribution b | - | - | - | - |

| Replacement (old animal)b | - | - | - | - |

| Replacement (young animal)b | - | - | - | - |

a) The bull’s live weight before slaughter was 280 kg while the average live weight of the heifers was 230 kg. The average carcass rate was 57%.

b) These aspects of management decision were not undertaken in this study due to time constraint. In practice, such decisions will take a longer period of time to accomplish before the results can be realized.

5. Conclusion

Animal waqf can be an innovative model of rural economic system with a focus on animal farming to help the poor and the needy to start off their livelihood, especially in raising animals for food. It is a system of detention of the object of waqf for an indefinite production of its benefits based on the maintained animal unit equivalents (AUE). The most important feature of AUE waqf unit is measurable quality and quantity of animals that are professionally managed by a farm manager, who may or may not be expert in shariah matters. For a conventional manager, a shariah-compliant standard operating procedure and check list will suffice. In other words, it is not necessary for a farm manager to have the knowledge of waqf or shariah law but his/her management activities must abide the by shariah-compliant checklist prepared by the Waqf Unit.

6. References

- Abdel Mohsin, M. M. (2019), “Waqfintech and Sustainable Socio-Economic Development”, International Journal of Management and Applied Research, Vol. 6, No. 3, pp. 130-141. https://doi.org/10.18646/2056.63.19-009

- Abdel Mohsin, M. M. and Muneeza, A. (2019), “Integrating Waqf Crowdfunding into the Blockchain: A Modern Approach for Creating a Waqf Market”, in: Oseni, U. A. and Ali, N. (Ed.), Fintech in Islamic Finance Theory and Practice, London: Routledge, pp. 266-280. https://doi.org/10.4324/9781351025584

- Abdullah, M. (2019), “Waqf and trust: the nature, structures and socio-economic impacts”, Journal of Islamic Accounting and Business Research, Vol. 10 No. 4, pp. 512-527. https://doi.org/10.1108/JIABR-10-2016-0124

- Abu ‘Abdullah Muhammad bin Ismail al-Bukhāry (d. 256 H). Al-Jāmi’ al-Sahīh. Al-Juzu’ al-Awwal. Al-Qahērah, Misr: Al-Matba’ah al-Salafiyyah.

- Al-Baihaqi, Abu Bakr Ahmad bin al-Husain bin ‘Ali (d. 457 H). Al-Sunan al-Kubrā lil-Baihaqī (al-Juzu’ al-Sadis, Kitab al-Waqf, Hadith no. 11886-11893, pp. 262-264). Beirut: Dar al-Kutub al-‘Ilmiyyah.

- Al-Bujairmi, Sulaiman bin Muhammad bin ‘Umar (d. 1221H). Al-Bujairmi ‘ala al-Khatib. Juzu’ 3. Beirut: Dar al-Kotob al-‘Ilmiyyah.

- Al-‘Imrāni, Abu Hussain Yahya bin Abu Khayr bin Sālim (d. 558 H). Al-Bayan fi Madzhab Imam al-Shāfi’e. Jilid 8, Kitab al-Waqf. Dar al-Manhāj.

- Al-Juwaini, ‘Abdul Malek bin ‘Abdulah bin Yusof (d. 478 H). Nihāyat al Matlab fi Dirāyat al Madzhab. Juzu’ 7. Beirut, Lebanon: Dar al-Kotob al-‘Ilmiyyah.

- Al-Khassaf, Abu Bakr Ahmad bin ‘Amru al-Syaibāni (d. 261 H). Kitab al-Ahkām al-Awqāf. Al-Qāherah: Maktabah al-Thaqofah al-Deeniyyah.

- Al-Nasāi’, Abu ‘Abdul Rahman Ahmad bin Shuib (d. 303 H). Al-Sunan al-Kubrā lil-Nasāi’ (Kitab al-Ihbās, Hadith no. 6391-6395, pp. 138-140). Beirut, Lubnan: Muassasah al-Risalah.

- Al-Syarwāni, A. H. and Al-‘Ibādi, A. Q. (n.d.). Hawāsyi Tuhfat al-Muhtāj bi Sharh al-Manhāj Juzu’ 6. Al-Bābīal-Hilbī, Egypt: Matba’ah Mustofa Muhammad.

- Al-Syatri, Sa’ad bin Nasir bin ‘Abd al-‘Aziz (2008). Syarh al-Umdat al-Ahkām (Jilid 1, Kitab al-Zakat, Hadith no. 181, p. 380), al-Riyadh: Dar Kunuz Isybīliā li al-Nasyr wa al-Tawzi’.

- Al-Nawawiy, Abu Zakariyya Yahya bin Sharfin (d. 272 H). Radhaut al-Tholibin. Juzu’ 4. Al-Riyadh: Darul ‘Aalam al-Kotob.

- Al Shafi’e, Imam (d. 204 AH). Al Umm. Vol. 5. Al Mansurah: Dar al Baida;

- Al-Quzwaini, Abu al-Qāsim ‘Abdul Karim bin Muhammad bin ‘Abdul Karim al-Rāfi’e (d. 623 H). Al-’Aziz Sharh al-Wajīz (Sharh al-Kabir). Juzu’ 6. Beirut, Lebanon: Dar al-Kotob al-‘Ilmiyyah.

- Almarri, J. and Meewella, J. (2015), “Social entrepreneurship and Islamic philanthropy”, International Journal of Business and Globalisation, Vol. 15, No. 3, pp. 405–424. https://doi.org/10.1504/IJBG.2015.071901

- Global Wakaf (2016), Cash Waqf for Humanity, translated by: Esa Khairina Husen [Online], available from: https://www.globalwakaf.com/en/berita/read/14/cash-waqf-for-humanity [Accessed on 1 July 2020].

- Ibrahim, Yahya bin Muhammad al-Amin al-Hassan (2007). Ahkām Bahīmah al-An’ām fi Ghair al-‘Ibādāt. Risalah Muqaddamat li Nail Darjah al-Mājestar fi al-Fiqh. Kuliah al-Shariah fi Riyadh, Qism al-Fiqh, Jāmi’ah al-Imam Muhammad bin Sau’d al-Islāmiyyah, al-Mamlakat al-‘Arabiyyah al-Sa’udiyyah.

- Ibhraim, M.R.; Niteh, M.Y. and Ahmad, M. (2016), “Sistem Penternakan Haiwan Secara Pawah: Permasalahan Dari Sudut Syariah (Pawah farming system from Sharia perspective)”, e-BANGI, Vol. 13, No. 4, pp. 123-132.

- Iman, A. H. M. and Mohammad, T. S. H. (2014), Waqf Property: Concept, Management, Development and Financing. Skudai: Penerbit UTM Press.

- Iman, A. H. M. and Mohammad M. T. S. H. (2017). “Waqf as a framework for entrepreneurship”, Humanomics, Vol. 33, No. 4, pp. 419-440. https://doi.org/10.1108/H-01-2017-0015

- Ismail, M.Y. (1982), “Tradition and Change in Aril, A Siamese Village in Kelantan”, The Australian Journal of Anthropology, Vol. 13, No. 3, pp. 252-263. https://doi.org/ 10.1111/j.1835-9310.1982.tb01235.x

- Johnson, O. (2020), A Modern Approach to Entrepreneurship and Small Business Management. New York: Wilford Press.

- Muhammad ‘Arafah al-Dusuki (d. 1230 H). Haasyiah al-Dusuki ‘ala Syarh al-Kabir (Jilid 4). Misr: Dar al-Ahyaa’ al-Kutub al-‘Arabiyyah.

- Mulyaningsih H.D., Ramadani V. (2017), “Social Entrepreneurship in an Islamic Context”, In: Ramadani V., Dana LP., Gërguri-Rashiti S., Ratten V. (eds) Entrepreneurship and Management in an Islamic Context. Cham: Springer. https://doi.org/10.1007/978-3-319-39679-8_10

- Rashedul Hasan and Abu Umar Faruq Ahmad (2019). Cash Waqf Crowdfunding Model for SMEs. In Abdul Rafay (ed.).Handbook of Research on Theory and Practice of Global Islamic Finance. Hershey, PA, USA: IGI Global, 338-354. https://doi.org/10.4018/978-1-7998-0218-1.ch019

- Ritchie, H. and Roser, M. (2017), Meat and Dairy Production, [Online] Available from: https://ourworldindata.org/meat-production [Accessed on 8 July 2020]

- Rostron, K. I. (2015), “Defining the Social Enterprise: A Tangled Web”, International Journal of Management and Applied Research, Vol. 2, No. 2, pp. 85-99. https://doi.org/10.18646/2056.22.15-007

- Shaikh, S.A., Ismail, A.G. and Mohd Shafiai, M.H. (2017), “Application of waqf for social and development finance”, ISRA International Journal of Islamic Finance, 9 No. 1, pp. 5-14. https://doi.org/10.1108/IJIF-07-2017-002

- Sherifah O. M. D. and Marhanum C. M. S. (2019), Cash waqf for Entrepreneurship Development, in: Abdul Rafay (ed.). Handbook of Research on Theory and Practice of Global Islamic Finance. Hershey, PA, USA: IGI Global, 290-305. https://doi.org/10.4018/978-1-7998-0218-1.ch016

- Shahbandeh, M. (2020), Number of ruminant worldwide from 2012 to 2020 (in million head). [Online] Available from: https://www.statista.com/statistics/263979/global-ruminant-population-since-1990/ [Accessed on 6 July 2020].

- Shulthoni, M.; Saad, N.; Kayadibi, S. and Ariffin, M. (2018), “Waqf Fundraising Management: A Proposal for A Sustainable Finance of the Waqf Institutions”, Journal of Islamic Monetary Economics and Finance, Vol. 3, pp. 153 - 178. https://doi.org/10.21098/jimf.v3i0.776

- Thornton, P. K. (2010), “Livestock production: recent trends, future prospects”, Philosophical Transactions of the Royal Society B: Biological Science, 365, No. 1554, pp. 2853–2867. https://doi.org/10.1098/rstb.2010.0134

- Wangchuk, K.; Wangdi, J. and Mindu, M. (2018), “Comparison and reliability of techniques to estimate live cattle body weight”, Journal of Applied Animal Research, Vol. 46, No. 1, pp. 349-352, https://doi.org/10.1080/09712119.2017.1302876

- World Bank (2016), A Year in the Lives of Smallholder Farmers, [Online] Available from: https://www.worldbank.org/en/news/feature/2016/02/25/a-year-in-the-lives-of-smallholder-farming-families [Accessed on 8 July 2020].

- United States Department of Agriculture (USDA) (2003), Natural Resources Conservation Service (NRCS) National Range and Pasture Handbook. US: USDA.

- United States Food Drug Administration (USFDA) (2019), The Cattle Estrous Cycle and FDA-Approved Animal Drugs, [Online] Available from: https://www.fda.gov/animal-veterinary/product-safety-information/cattle-estrous-cycle-and-fda-approved-animal-drugs-control-and-synchronize-estrus-resource-producers [Accessed on 8 July 2020].